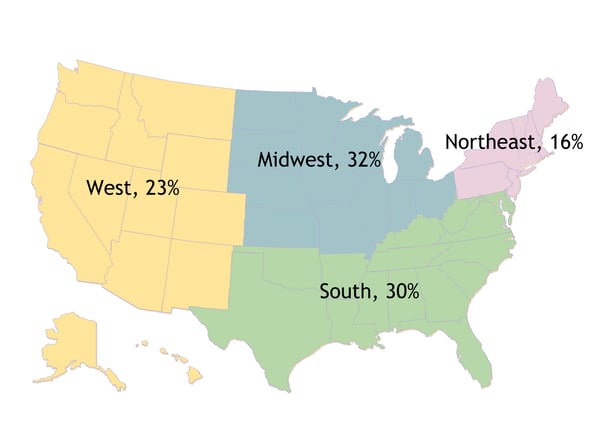

.png)

(reprinted with permission from NCEO.org)

blog.png?width=790&height=444&name=12%20bogus%20reasons%20not%20to%20do%20an%20esop%20(and%207%20good%20ones!)%20blog.png)

ESOPs can be an ideal business transition solution for many business owners, providing a way to preserve their legacy with employees and the community, get a fair price, retain a role in the company if they like, and get unmatched tax benefits in the process.

But while ESOPs are not right for many companies, over the years, we at the NCEO have heard a lot of unconvincing or downright incorrect reasons not to do an ESOP. Unfortunately, too many business owners decide not to do an ESOP based on these bogus rationales. Here at the NCEO, our goal is not to convince anyone to implement an ESOP but to help people make a well-informed, sensible decision. With that in mind, below is a list of twelve reasons you might have heard about why not to do an ESOP that are just wrong, followed by seven very legitimate ones.

"Regardless of the offers, it was more important that we ensured our firm's culture and legacy remained intact. Doing things The Graham Way has served us well for more than 60 years. This ESOP is an investment in the next 60 years."

—Bill Graham, The Graham Company

Learn how employee ownership can play a roll in The Great Game of Business

Twelve Bogus Reasons Not to Do an ESOP

1. ESOPs cost too much:

The question really is whether ESOPs cost too much relative to other ways to provide for business liquidity, the most common reason for setting up an ESOP in a closely held company. An ESOP will probably cost $80,000 to $250,000 (mostly in the lower part of this range) to set up and run the first year and, for most companies with less than a few hundred people, $20,000 to $30,000 annually. Selling to another company involves tens of thousands of dollars in legal, accounting, and valuation fees, plus, if there is a broker, as there often is, another few to several percent of the transaction. Only half the companies that are large enough to do an ESOP, but try to sell to an outsider, end up being sold, and almost always with a variety of contingencies. There is no broker in an ESOP, so there are none of those fees. And the sale is not contingent. Sellers to an ESOP can get substantial tax benefits unavailable in other sales. So for most sellers of all but the smallest companies, an ESOP is actually much cheaper than selling some other way. Setup fees can be more in a few cases, depending on financing sources and whether independent fiduciaries are required.

2. ESOPs are too complicated:

Again, the question is, compared to what? As our article Are ESOPs Really More Complex Than Other Ways to Sell a Business? explains, selling to another buyer is an enormously complex process, usually carrying a variety of contingencies. ESOPs are complex too, but not more so.

3. The ESOP cannot match what other buyers will offer:

The ESOP will pay what an appraiser determines a financial buyer would pay (such as an individual investor or private equity company), but not what a synergistic buyer (such as a competitor) might offer. However, the ESOP pays cash; outside buyers often pay partly in cash and partly in an earnout. There may also be financing or personal contingencies on the sale (such as requiring the seller to stay or leave). Other buyers also cannot offer the opportunity the ESOP does for the seller to defer capital gains tax on the sale. As explained in Ownership Transitions: ESOPs Compared to Other Strategies, factoring all this in, only a small minority of sellers can get a meaningfully higher price selling to another buyer.

4. Management must share financial information and governance with employees:

There is no requirement to share financial information. Companies need only provide annual account statements indicating the total value of the account, vesting status, and stock value. The most effective ESOP companies are "open book," but it is their choice to do that. The ESOP is governed by a trustee appointed by the board. Employees get involved in management or corporate issues only if the company wants them to do so.

5. The employees don't have the funds to buy the company:

Employees in an ESOP do not use their own funds to buy the company. ESOPs are funded by corporate pretax contributions to the employee stock ownership trust. There can be annual discretionary cash contributions to buy shares each year, or the trust can borrow money to buy shares, with the company making tax-deductible contributions to pay off the loan.

6. ESOPs are too risky for employees:

ESOPs are not diversified, at least in their early years. But having an ESOP does not preclude the company from having a 401(k) plan or any other kind of retirement plan. The company may, at least temporarily, suspend any match or contribution to these other plans, but employees can still make contributions. Employees do not pay for the stock in the ESOP, so they only risk potential gains. In long-term ESOPs, employees can start to diversify within the plan.

7. ESOPs work only in certain industries:

Name any industry, and there are ESOP companies in that industry. See ESOPs by the Numbers for more information.

8. Bank credit for an ESOP loan is not available:

ESOP loans have a very low default rate, so banks that have some experience in this area typically will view them more favorably than other highly leveraged transactions. If bank credit is not available, however, sellers can finance the sale directly by taking a note, with the ESOP paying an equivalent arms-length interest rate.

9. Companies have to keep repurchasing their own shares:

That is true in closely held companies. By law, at some point after ESOP participants leave a closely held company, the company has to make sure the shares get repurchased, either by the company or the ESOP (or, less often, someone else). But any closely held company has a 100% repurchase obligation all the time; ESOPs are no different. If employees buy shares directly, such as in a management buyout, they too will want liquidity for their shares at some point. The difference is that with ESOPs, repurchase occurs in smaller bites every year; with other ownership arrangements, when owners want to sell, the company either finds another buyer or liquidates.

10. Younger employees are more concerned with short-term cash than with potential retirement benefits:

Extensive academic research shows demographics (age, seniority, education, income, and position) are not predictors of employee reactions to ownership.

11. ESOPs are difficult for employees to understand and appreciate:

They can be if companies don't make the effort. But they can be explained if you do. And if you create a true ownership culture at your company, it will perform significantly better.

12. ESOPs companies do not perform well:

The evidence points in exactly the opposite direction. (See our article Key Studies on Employee Ownership and Corporate Performance for details on this finding.) ESOP companies grow 2% to 3% faster than would have been expected without an ESOP, and have lower turnover and 2.5% higher productivity. Profit data per se are not available for closely held companies because they don't disclose it, but there are lots of proxies. The National Bureau of Economic Research has concluded that ESOPs are significantly correlated with economic performance. The relationship is not automatic, however. Companies that combine ESOPs with what we call an "ownership culture" (they share financial information and get people involved in work-level decisions) grow 6% to 11% per year faster than would have been expected; companies with top-down cultures grow more slowly post-ESOP than would have been expected. In other words, an ESOP works if part of an overall culture, not all by itself. Just having the culture without the ownership, by the way, doesn't work very well either.

Seven Good Reasons Not to Do an ESOP

1. There is a synergistic buyer willing to offer a very substantial premium.

If price is the primary concern for an owner, and there is a synergistic buyer willing to pay a significant premium, an ESOP may be the wrong choice. Several factors come into play here. First, the seller must be looking to get out entirely. Some sellers only want to sell part of their ownership, or there may be one or more owners who want to sell and one or more who do not. Second, the premium must be large enough to offset the ability of a seller to an ESOP that meets the basic requirements (the ESOP owns at least 30% after the sale, the company is or converts to a C corporation, the company is closely held, and the owner has held the stock for three years) to defer taxation on the gain by reinvesting in other securities. Third, the buyer's offer must not contain unacceptable contingencies or uncertain financing.

2. The company is too small.

ESOPs typically cost $80,000 or more even for very small companies to set up. For very small companies (typically less than 10 to 15 employees), these costs may be greater than potential tax benefits. If the company is an S corporation, rules aimed at preventing a small number of people from getting the bulk of the ESOP benefits may make an ESOP impossible even if all employees are in the plan. The company could convert to C status, however

3. There is no successor management.

If the seller is the key manager, capable successor management must be in place to obtain an outside loan as well as to help assure that the company will be able to pay for the plan over time.

4. The payroll is not large enough.

In rare cases where the value of the company relative to the size of the payroll is very large, limitations on how much can be contributed annually to the ESOP may make it impractical to buy a substantial percentage of the company.

5. The company is not profitable enough to afford the contributions.

When an ESOP is buying out an owner, the cost is a non-productive expense. Companies need to assess whether they have the available earnings for this. ESOPs are not usually good choices for struggling companies.

6. Management is not comfortable with the idea of employees as owners.

While employees do not have to run the company, they will want more information and more say. Unless they are treated this way, research shows, they may be demotivated by ownership.

7. Family members or specific executives want a major share of the company.

An ESOP cannot be used to transfer ownership to specific people. ESOP rules require that contributions be allocated based on relative compensation up to (in 2018) $275,000 or some more level formula. Moreover, everyone who has worked for 1,000 hours in a 12-month period must be in the plan (with certain exceptions, such as employees covered by a collective bargaining agreement). Family members and more-than-25% owners also cannot get allocations of any shares subject to the capital gains deferral. Individuals can buy or, within reasonable limits, be given shares outside the ESOP, or be given equity rights such as stock options or stock appreciation rights. If the goal is to transfer most of the ownership to a select group, then, an ESOP is not appropriate.

Why Your Advisors May Be Misleading You

Having read this, you may wonder why your advisors would have given you information that may have been misleading. There are a few possible reasons:

1. They have limited knowledge:

While the honorable thing to do when you have limited information is to tell your clients that they may want to get some other opinions from people more knowledgeable in the field, there is a natural tendency to want to seem more expert than you actually are (think about all those TV pundits who happily opine about all kinds of subjects they know little about).

2. They had a client or two with an ESOP that did not work out:

Personal experience has a strong emotional pull. The stories we know can be much more powerful than reams of data or expert opinion.

3. They fear losing you as a client:

This is especially true if the advisor is a business broker. They make their money by finding a buyer other than an ESOP. ESOP sales do not (and should not) involve finders fees, which usually are a percentage of the transaction charged for locating a buyer. I have had more than one broker tell me that even though their client was a very good ESOP fit, they could not recommend an ESOP. Brokers and investment bankers can be paid, however, for actual services they provide, such as finding capital, feasibility analyses, and transaction advice. Other advisors, such as attorneys and accountants, may worry that if you do an ESOP, you will seek specialized advisors, not them. It's not that most of these people are intentionally misleading you, it's just that the pull of their own self-interest may make them see the world differently. Our experience at the NCEO is that most professional ESOP advisors are willing to work closely with existing advisors, and most welcome the opportunity to provide to the existing advisors the specialized knowledge required.

This is not to say that your advisors are acting against what they know to be your best interests. But ESOPs are a highly specialized area, and there is a lot of misinformation out there. So it's easy to make mistakes. I hope this article will help you avoid some of them.

.png)