.png)

Unfortunately, it’s not just decades-old companies that hoard information or run out of cash. It happens to companies of all shapes and sizes every day. And sometimes they’re even being told it’s good for their business. If that sounds crazy to you, you’re right. It’s crazy. And what about schools and innovation centers that teach a generation of young entrepreneurs what they need to do to succeed but don’t include classes on managing cash?

We learned the following lesson from Doug, a serial entrepreneur, and author who now teaches entrepreneurship classes to college students. Doug told me about the first class he taught and that he started it with a question. He asked his students what the definition of profit was. To guide them, he offered two possible definitions:

-

-

Definition 1: profit represents value.

-

Definition 2: profit represents cheating the customer.

-

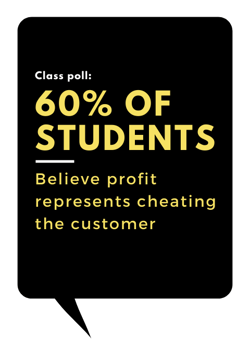

When Doug asked for a show of hands for each definition, he was shocked to see that about 60 percent of the students chose the second definition. He knew then that he had a lot of ground to cover that semester to explain what profit really was. At the same time, Doug began informally polling other people by asking them the same question—at conferences and cocktail parties—and he found that they, too, chose the second definition more than half the time. He began to wonder if there was something in the water. Why did people think profit was such a bad thing?

When Doug asked for a show of hands for each definition, he was shocked to see that about 60 percent of the students chose the second definition. He knew then that he had a lot of ground to cover that semester to explain what profit really was. At the same time, Doug began informally polling other people by asking them the same question—at conferences and cocktail parties—and he found that they, too, chose the second definition more than half the time. He began to wonder if there was something in the water. Why did people think profit was such a bad thing?

In the fifteen years since then, Doug has continued to start every semester with that same question. Incredibly, he found that he got roughly the same response every time. It got him worried about the future and what kids were learning. What stunned him the most was that these were business students who were answering the question this way. Doug eventually co-authored an article that was published in a prominent academic journal. The article reported the results of his surveys and suggested they might be indicative of a knowledge gap in today’s society about what profit is and what it’s used for.

Teach people the rules

To me, it’s a clear indicator that people, especially young people, aren’t being taught the rules, and they’re putting their lives, let alone their businesses, at risk. I’ve witnessed this trend firsthand. One great example is that of Jesse, a bright young woman who happened to know me through one of my daughters. Jesse and her husband, Sam, had started an e-commerce site in 2013, which they were operating out of a business incubator based near a major university. The business had an interesting niche in that it catered to home designers and renovators, and interest in the business was booming. She had heard that I had made some angel investments in young companies like hers, so Jesse called me up one day in hopes that I would be willing to review and possibly invest in their venture.

During that phone call, I learned that both Jesse and Sam had run businesses of their own. Jesse had a ton of experience in the marketing world as well as interior decorating and design. Sam, who had graduated from college with a degree in finance, had been working in the banking industry for several years, where he had been part of several mortgage company start-ups. It was clear they already had a lot of combined entrepreneurial experience. It was also hard to ignore the passion in Jesse’s voice when she explained what her business did and where she wanted to take it. The idea had come from the fact that Jesse’s friends and family kept asking for advice on how they could remake their homes. But whenever Jesse went to buy any supplies, she was forced to pay marked-up retail prices; she couldn’t get access to better wholesale deals because she was just an independent contractor. Her business idea was based on

selling products, supplies, and designs to other design contractors at reasonable prices. It seemed an interesting concept, so I agreed to meet with Jesse and Sam to learn more about how they were building their business.

Don't evaluate your company on potential alone

Just a few minutes into our conversation, I immediately knew something was wrong. Jesse and Sam’s pitch was entirely aimed at raising money in exchange for an equity stake in their business. All they talked about was how much they thought the pre-money valuation of their business was. What was missing was any real discussion about how they would earn a profit and generate cash. So, when they told me they thought their business was worth more than $2 million, based purely on the advice they had been given, I just about had a coronary. They were evaluating their company based on potential alone.

When I looked at their financials and their projections, the story only got worse; there were red flags everywhere. It was like looking at a business plan from outer space. Early on, they had done a good job of managing their expenses—they had broken even in their first year—which their coaches at the incubator told them was an amazing accomplishment. But things then went downhill. Their coaches told them they were in a hot industry and had to outgrow their competitors if they wanted to be successful over the long term. Jesse and Sam were coached to model themselves after a neighboring business in the incubator that was now planning a move to New York City after that business had landed a superhigh valuation by investors.

Where to spend your dollars

Jesse and Sam wanted to ramp things up. They wanted to spend more and more money by hiring employees and investing incredible sums in their marketing campaigns. They had started the business with their savings, but they planned to quickly increase their spending after they secured a $50,000 loan from the Small Business Administration.

What I couldn’t get my head around was how much they wanted to spend on online marketing and advertising: thousands of dollars a month. I had never seen another business in which sales and marketing expenses were more than 20 percent of their sales. But projected marketing expenses for these kids accounted for 90 percent of their cost of goods sold. In other words, most of the costs of running their business would be tied up in buying online advertising to try to win new customers.

“We constantly kept tabs on what our larger competitors were doing and how much they were growing,” Sam told me. “We kept spending more to try to keep up with them. We really wanted to push and scale up as fast as we could.”

“We had our eyes on the prize,” Jesse said.

What they didn’t realize was that they had entered an unsustainable rat race they couldn’t hope to win by trying to spend as much as they could in online advertising. When you have to spend all your money up-front just to get customer leads that only have the promise of future revenue, you’ll burn through your cash faster than you could ever imagine. They didn’t realize they were caught up in what was as close to a Ponzi scheme as I’d ever seen. They’d been brainwashed to believe that everything revolves around social media sites such as Facebook and Instagram. They fell into the trap of running their business based solely on the notion of how many hits their website got or where they were placed in a search result. They had to invest more and more money to stay ahead of their competitors on search results. But those competitors were also using the same strategy, so they were engaged in an arms race that would likely lead to mutually assured destruction. The social media companies would make out just fine no matter what happened.

I know that’s part of running the business these days, but it’s not the whole big picture. And what happened is these kids ended up spending all their time trying to figure that part out and were not focused enough on building and running their business. They didn’t know the rules.

Debt is devastating

If they followed their plan, they would outrun their coverage by spending too much, too fast, which would leave them in a disastrous position. It was clear to me they were going to soon face a severe cash crunch. They would go through every circle of Dante’s hell to acquire money to grow their business. But why? They didn’t realize that path would suck all the oxygen out of their bodies, as well as their children’s, and they could lose their house. If they didn’t land an investor willing to put money into the business, they might not even survive the year. But even if they were to secure some cash in the short term, I wasn’t convinced they could execute their long-term vision, especially if they had to answer to an outside investor. Most people overlook how devastating debt is. It erodes security and protection in a way that makes people do crazy things.

Despite the fact that these two young people had a couple of young kids at home, they were ready to mortgage their house and everything they had to make their business a success. I really wanted to help them—but only if they were willing to learn there was a better way to run their business.

They were focused more on creating a million-dollar company than they were on putting food on the table or being able to go home after work and watching their kids play basketball. They didn’t realize how much time they would spend meeting with their investors and explaining how they were going to hit their numbers. Many failed entrepreneurs think they can grow out of their problems. They need to learn to do more with less instead.

So I asked them, “Why are you doing it this way? Why are you so focused on bringing in outside investors to grow so fast? Don’t you want to raise your family and have a life?”

Jesse and Sam explained that it was their mentors and other startup entrepreneurs at the incubator who told them this was the way they needed to build their business. Their advisers wanted them to outrun their competition. But did their teachers also explain the kinds of emotional strings that come attached to borrowing money?

I think there is a big cognitive gap here. Sam and Jesse didn’t realize that misery and pain goes along with borrowing money from outside investors. They were not aware they would have sleepless nights worrying about whether they could make their payroll and whether they would let down the people who lent them the money. It can be a horrific experience. Just picture yourself in a situation where you’ve borrowed money from your parents’ retirement account, and you can’t pay them back. It is why debt can become a suffocating black hole.

I think there is a big cognitive gap here. Sam and Jesse didn’t realize that misery and pain goes along with borrowing money from outside investors. They were not aware they would have sleepless nights worrying about whether they could make their payroll and whether they would let down the people who lent them the money. It can be a horrific experience. Just picture yourself in a situation where you’ve borrowed money from your parents’ retirement account, and you can’t pay them back. It is why debt can become a suffocating black hole.

Apparently, they had been scouring the country, traveling multiple times to cities such as New York, Saint Louis, and Kansas City in search of investors willing to back their venture. Having struck out to that point, they were now expanding their search by talking to potential investors on the West Coast as well. “We had such a strong vision for what we wanted to build,” said Jesse. “But we were frustrated because it didn’t seem like we could get traction with investors.

Taught to Fail

We didn’t know why we couldn’t get them to see our vision.” I was stunned. It was clear to me that despite their experience in running businesses, they couldn’t even spell equity. Their coaches had somehow convinced them that building an internet-based business was different, that the old rules of building a business needed to be thrown out in favor of something new tied to the internet. It was as if the dot-com era was happening all over again.

The truth was, however, that they were being taught to fail. While that might sound harsh, I was completely baffled by the fact that these young entrepreneurs believed their ultimate goal was to have investors value their business as high as possible and then scale up as fast as they could to be able, eventually, to pay off those investors. They might even be forced to sell their business, something that wasn’t part of their long-term plan.

What really angers me is that this same model is being taught to a generation of entrepreneurs through schools and so-called incubators and innovation centers that supposedly exist to nurture and support young businesses. But to what end? That’s why most companies never make it past their fifth anniversary.

What I can’t understand is why people are in a rush to give away so much of the equity in their company to an outside investor if it isn’t necessary. They are, essentially, buying bosses who will climb on their backs and drive every decision they need to make. They will work the same number of hours to grow the business, but the upside won’t belong to them any longer; it will be the outside investors who reap the benefits of the entrepreneurs’ hard work.

It’s as if the tried-and-true rules of running a business are being forgotten in favor of something else. But the financials don’t lie. They are your guides to understanding how fast you can grow. Today’s entrepreneurs are being taught to ignore those facts.

Something like only 10 percent of companies reach the $1 million revenue mark. And yet so many young business entrepreneurs are encouraged to race against each other to build the next Amazon or Facebook, and this advice is killing companies and wasting a lot of capital as a result. I really liked Jesse and Sam. They had grit. But that put me in a tough position. It was clear that without an infusion of cash, their company would soon be on its last legs, maybe in less than ninety days. Yet I felt they didn’t need an investor as much as they needed someone to give them a practical education.

Practical education

While they wanted me to consider giving them some money in exchange for an equity stake in the company, I didn’t want to take the direct investment route. Instead, I offered to loan them unsecured money at a superlow interest rate they could then use as collateral to go back to their bank and get a larger loan. I did some homework on their financials and came up with an amount I figured would help them right their ship. Because the loan was unsecured, I knew most banks would be willing to lend up to three or four times that amount because, if something were to go wrong in the business, the banks would get first dibs on reimbursement.

Before I lent Jesse and Sam the money, they had to make some changes in their business model. That started with addressing the company killer staring them right in the face: lack of cash flow. They faced a fundamental problem in that their vendors had asked them to pay cash for all their products at the time they ordered them. But they wouldn’t receive any money from their customers for some thirty or sixty days after they shipped the product to them. It was an unsustainable model unless they could get better terms from vendors they could pay later, preferably after their customers had paid them. They were also planning to move the business into a new location, but I told them the cost of the new building would put even more pressure on their cash flow.

I think they were surprised, maybe even disappointed, by my decision. But I really wanted them to learn what it meant to run their business rather than just run around looking to hand their company over to investors. I had walked away from making investments before unless the entrepreneurs were willing to listen and transform their way of thinking about their business. I wanted Jesse and Sam to learn how to grow slow and smart. I wanted them to borrow money to help grow the business, not go out of business by continuing to dump their cash into a bottomless pit. They wanted to have this fast-growth internet company. I wanted them to grow out of their house. Rather than becoming their angel investor, I was hoping to serve as their guardian angel.

Change to deal with your challenges

As we talked through my plan, I could see Jesse and Sam’s eyes opening. And to their credit, they jumped into making changes to deal with their challenges. Just a few months later, they had a lot of exciting updates to share with me.

- They had successfully negotiated better terms with seven of their top ten suppliers. They also called up their credit card company and asked for extended payment terms so they could pay their bill in forty-five to sixty days instead of thirty, which also gave their cash flow some much-needed breathing room.

- They went to work on managing their expenses better. They slashed their monthly marketing budget basically in half. They also scrapped the plan to move to the new office they were considering, which would have cost $7 a square foot plus the added cost of building out the space to their needs. After some research, they found another option with a landlord who offered them office space at $2 a square foot.

- Jesse and Sam learned from negotiating with their suppliers that they could get better pricing—as much as a 10 percent discount—if they had a brick-and-mortar retail location. Apparently, many suppliers offer those discounts as a way to balance the equation with pure e-commerce retailers, who can then offset any investment they might make in a physical space with the savings they gain from discounts on the costs of their products.

There was also a question of their profit margin. They had two kinds of orders: small parcel orders and freight orders, with freight orders making up about 51 percent of their sales.

Because their order system didn’t automatically give them the detailed information they needed, they put some effort into analyzing their orders to understand how much money they made on each type. It was then that they realized for the first time that they earned far more profit—about 15 percent more—on their small parcel orders than on freight sales.

- They adjusted their marketing strategy to focus more on their small parcel products, while also looking for ways to reduce the shipping costs of all of their orders.

- Then they tackled the rigors of forecasting by coming up with detailed, monthly cash-flow projections to see how the changes they made would affect their ability to make a profit while generating cash over the long term.

“We were so naive,” Jesse told me. “It was amazing how much time and energy we were putting into traveling around and talking to investors rather than running our business. But when we switched our mindset to work on growing slow and smart, we became profitable and retained ownership in our company. We’re still learning, but it’s hard to imagine where we would be today if we had brought on someone different as an investor. We feel like we’re finally on our way.”

It’s unbelievable to see how much Jesse and Sam changed in just a year with the encouragement to stick to the basics of business. They have become empowered by learning to ask their suppliers and customers for help, something they didn’t even know they could ask for. My hope is that their eyes have been opened and that they now have the tools and the scorecard to control their own destiny or to at least create the kind of business that gives them the balanced and happy life they want.

Now what?

In a more recent phone call, Sam sounded upbeat and positive about where the business was headed. They had hired employees and were nearing completion of their brick-and-mortar store. Just as importantly, they had boosted their margins another 10 percent and got their cash flow under control. Perhaps most impressive to me was the fact that they nailed their forecast with 96 percent accuracy, which told me that they were listening to the right music.

Of course, there were still challenges to overcome. “Our biggest killer is the cost of freight,” Sam told me. “Because we ship to different areas of the country, we have learned that not all the shippers are good at working with furniture, so we’ve also had to work around damages and returns from customers.” The good news, however, was that he and Jesse still owned 100 percent of the business. They were working hard for the benefit of themselves and their children.

After sharing his updates with me, Sam told me he had to run. He was on his way to coach his kids’ basketball team. That, I told him, was worth a million bucks all on its own.

I think the trap for so many entrepreneurs may be that they find themselves building a business rather than a life. They need to take both into consideration. To do that, they need to learn business and financial literacy skills to understand and evaluate the opportunities that present themselves.

I saw another example of what young entrepreneurs are being taught today when I was asked to invest in a technology start-up. The entrepreneur had developed what he thought was an exciting app that everyone would want. He, too, enrolled in an incubator where the coaches immediately pushed him to borrow as much money as he

could from investors and banks—as well as his family and friends—so he could scale his app as quickly as possible. The instructors told him to swing big or go home. Well, that entrepreneur is still swinging, six years later, even though he now owes those investors and family members a total of $900,000. To his credit, he won’t give up. He still thinks he can turn things around. But all that money has to feel like a monkey on his back. The worst part is that he is still asking for more money—a lot more—because he thinks that’s what he needs to hit his business tipping point. Imagine that: a young guy in his early thirties, with a family, who already owes nearly $1 million—and he has no equity to show for it either! And this is what we are teaching young people these days about building a business.

Yet another story involves a young entrepreneur who used his family’s life savings to buy a candle factory. He had graduated from a business program at a major university and thought he knew how businesses were run and operated. So rather than start a new business, he saw an opportunity to turn around an existing operation, something

that would be far less risky. Unfortunately, what this entrepreneur learned after the deal closed was that the former owner had questionable financials. Rather than generating cash, the business was eating it for breakfast. Worse, the inventory numbers were all bogus, which meant the balance sheet was a fraud as well. Just a few years later, this

young entrepreneur had no choice but to declare bankruptcy. As part of the deal, he now has to pay something like $1,200 a month for the next twenty years to pay off his debt, all while trying to support his young family.

While this guy was obviously a victim of a con job by the seller, it does beg the question of whether he really understood the basic rules of business before he made the deal. Did he have the savvy to pore over the financials, or to even walk through and take a hard look at the inventory? “We did do some due diligence on the financials and our

attorneys did as well,” he told me. “What we did not anticipate is that our willingness to trust would be taken advantage of. Quite a lesson.”

My goal is not to blame the victim here but to point out that unless we teach our young entrepreneurs the basics of running a business—not simply advise them to borrow as much money as they can or grow as fast as they can—we’ll be staring at even more tragedies like this in the years ahead.

I can’t decide if I’m more sad or mad at the fact that I keep running into talented and energetic entrepreneurs who are just trying to fulfill the American dream but are becoming tragedies instead because they’re using the wrong system to run their businesses.

The good news is that when young entrepreneurs do learn the basics of putting the system in place, amazing things can result.

This is an excerpt from Change the Game, Chapter 4.

Get Your Copy today!

.png)